Today we get to the crux of the matter.

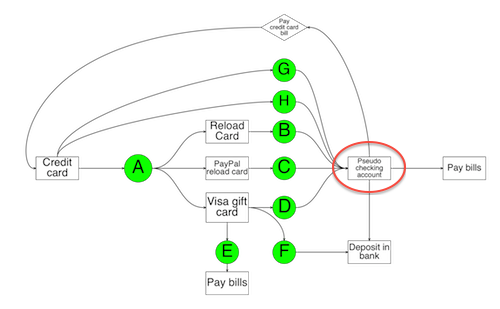

If manufactured spending is alchemy, turning credit card spending into cash, then the transformational step is certainly the loading of your pseudo-checking account.

where the magic happens…

So what is a pseudo checking account?

A pseudo checking account is a prepaid card that can be loaded by credit card in a number of ways. (We’ve already discussed using Visa gift cards, and reload cards,and we’ll get to the PayPal axis soon enough.)

Pseudo checking accounts were conceived of as a way to take advantage of err… As a way to bring the power of checking to the unbanked masses.

The idea is that those who do not have the resources to open bank accounts can simply register for a prepaid card and then use it to write checks and do online shopping. Sure, there are often a lot of little fees, but the fees are nowhere near as bad as at those check cashing places. (plus the prepaid cards drive their owners into establishments like Walmart and Target.)

The important thing, from a miles game player’s standpoint, is not the societal implications of such a product. The important thing is that the prepaid card can be used to transform credit card spending into cash equivalents (checks, money orders, and direct withdrawals to personal bank accounts.) This is really raison d’etre for manufactured spending

There are countless pseudo-checking accounts, and I will write about a few of them here, though my list is not exhaustive.

The big three (Bluebird/Serve/Redbird) are all from American Express, and they are mutually exclusive. (You can only have one of these at a time per Social Security number.)

Bluebird :(The old standby.)

Gestalt: This was a real game changer at one point: the first pseudo-checking account that allowed you to swipe reload the account with pin enabled Visa gift cards. Now it’s just sort of okay.

How to load: vanilla reloads (defunct), non-vanilla brand Visa card swipe reloads at Walmart. (swipe reloading means using your Visa gift card as a pin enabled debit card.)

How to liquidate: Use online bill pay to pay your bills, credit card and otherwise. (This bill pay feature is quite similar to using any bank’s online bill pay system, minus the recurring payments) , purchase money orders, or withdraw money directly to a linked bank account.)

Load limits: $1000 per day, $5000 per month- swipe reloads only.

Verdict: was a real trailblazer at one point but at this point it been eclipsed by newer developments.

Serve and Softbank Serve cards. (The big-box store avoidance card.)

Gestalt: This is my go to card. No other card is quite so easy to load up with manufactured spending with lots non-big-box-store-reloading-options as well as automatic loading options.

How to load: reloadables (reloadit cards, moneypaks), automatic online reloads (with both debit and credit cards), and swipe reloads with Visa gift cards at Walmart (non-vanilla)

How to liquidate: Use online bill pay to pay your bills, credit card and otherwise, purchase money orders, or withdraw money directly to a linked bank account.)

Load limits: $2500 a day via reload cards/swipe reloads, $5000 a month. Automatic on line loading of $1000/month via both debit card and credit card ($1500 each when enrolled in the softcard version of serve.)

Verdict: the most convenient card of all if you can find places to purchase reload cards with a credit card. This is a better option than bluebird by any metric, but not as cheap as Redbird…

Redbird (The cheapskate’s dream!)

Gestalt: this new kid on the block is a game changer! There is no cheaper way to manufacture spend if you have a Target handy.

How to load: You can load it fee free with your credit card at target! You can also swipe reload it with debit cards/Visa gift cards.

How to unload: Use online bill pay to pay your bills, credit card and otherwise, purchase money orders, or withdraw money directly to a linked bank account.

Load limits: $2500/day, $5000/month

For an excellent series on this new product (which I have not yet used.) please see here.

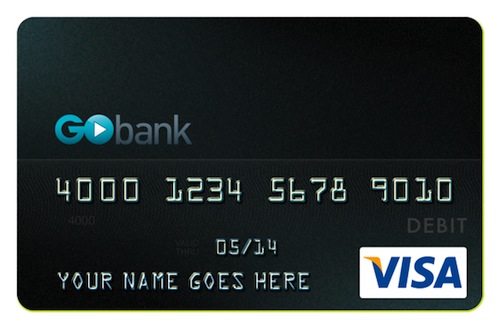

GoBank Card (The Pepsi to Bluebird’s Coke)

Gestalt: a useful adjunct to Bluebird/Redbird/Serve

How To Load: swipe reloads at Walmart, Moneypak reloads

How to unload: Use online bill pay to pay your bills, credit card and otherwise, purchase money orders, or withdraw money directly to a linked bank account.)

Load limits: $2500/day, $5000/month

T-Mobile prepaid card (a nice free adjunct)

Gestalt: I’ve never used this product but a little bird told me that it is possible to manufacture spend for free with this card using reloadits

How to load: load for free using reloadit packs. (Other options not useful for manufactured spending.)

How to unload: money orders, evolve money, (bill pay not recommended)

For a nice write up of this product see here.

My personal approach is to use the softcard version of serve, loaded with moneypaks, Credit card, and PayPal debit cards. In the end (despite my cheapskate nature) I place a high value on not going to big box stores to get my manufactured spending done.

I unload the products primarily with bill pay and direct withdrawals to my checking account.

I also have a Gobank card for back up, but I almost never use this anymore.

I am intrigued by the T-Mobile product, and though I really have no use for it now, may consider experimenting with it in the future.

And really no matter what you value the most (cheapness, convenience, the ability to use a certain gift card or reload card) picking at least one of these pseudo-checking accounts is the crucial step in converting all of your non-credit card spending into credit card spending.

And there are many products which I did not mention here. If there is one that you like using, please share it below in the comments.

9 Responses to “So Pseudo”