Sun Tzu observed that “if you know the enemy and know yourself, you need not fear the result of 100 battles.”

And as pat as it is to compare investing to war, it is also apt. For every investment is a transaction between a buyer and a seller, which means that every trade, on some level, is dualistic. You either win or you lose.

In my last post in this series I looked at the broad philosophical justification for dual momentum investing. Namely the empirical observation that momentum is everywhere, and the hypothesis that as long as humans are involved in markets, momentum is likely to persist. Performance chasing is just that essential to our make up.

So in this post I want to make like Sun Tzu and to consider my own chosen strategy’s weaknesses before entering into battle. For in battle there is no time for doubt. And since there is no strategy that does not contain weakness, it stands to reason that it is better to ponder any strategy’s faults in order to see trouble coming, and to react to it with calm rather than panic.

And so to begin this exercise let me lay out my fundamental assumptions about dual momentum. For without a doubt it is what I am sure of that is not in fact true that has the most potential for my own destruction.

Here then are my honest assumptions about the nature of capital markets and dual momentum investing that have informed my decision to adopt this strategy for my own tax exempt portfolio.

1. Since relative price momentum has existed everywhere that it has been studied, and has persisted long after it was first described, it is likely to persist into the future.

2. Absolute momentum (or timeseries momentum) is a form of trend following. As such by its very nature it must provide persistent and predictable downside protection.

3. Short-term treasuries are a risk-free asset.

So let’s come up with some counter arguments or hypothetical scenarios which would weaken my underlying assumptions and cause the persistent underperformance a dual momentum portfolio.

Hypothesis 1: Momentum Is Pervasive And Persistent in all markets.

Counter argument: The make up of the market is changing.

Although dual momentum has been present everywhere it has been looked for to date, markets are rapidly changing. Each year passive index funds claim a larger proportion of invested dollars (though at this point they’re still the vast minority.)

And if the performance chasing active investor is apt to perpetuate momentum by buying recent winners, shouldn’t the rebalancing of passive investors perpetuate the exact opposite? (Rebalancing should move in opposition to performance chasing, because by it’s very nature rebalancing means selling recent winners and buying recent losers. )

Furthermore the last few years have seen the rise of the Roboadvisers. If future decisions are to be made more and more by perfectly rational computer algorithms, and if momentum is an expression of human irrationality, then isn’t there a decent chance that the momentum effect will become ever more dilute with automation?

I have not been programmed to chase performance…

Takeaway: At this point the market is still very much driven by human decision-making, and active management. Given this, my feeling is that momentum continues to be a very good bet. But it’s worth always keeping an eye on the evolution of the market because the forces that drive market moves may change and at that point relative price momentum may become a bad bet.

Hypothesis 2: Absolute Momentum Protects Investors Against Big Drawdowns.

Counter argument: There are at least two exceptions to this rule.

For the most part bear markets are all similar versions of each other. There is a fundamental change in the marketplace that shocks the market, traders panic, volatility goes through the roof, and the stock market stairsteps downwards over the course of months and years. It reaches bottom, and then begins a gradual recovery in fits and starts.

And it is this classical version of a bear market that packs most of the returns beating punch in the dual momentum strategy. For although relative price momentum allows the investor to gain incrementally more during bull market periods, absolute momentum allows the investor to lose dramatically less during Bear market periods. Why? Because once the market starts stair stepping down, and the returns of the invested asset class over short-term treasuries during the look back period have been erased, then the investor switches fully into the safe asset of short-term treasures. In this way the dual momentum investor is safely on the sideline for most of the bear market (and a brief time at the beginning of the recovery.)

But when would such an approach not work? The answer is obvious:

In A Flash Crash.

A flash crash such as what occured on black Monday in 1987 is the worst case scenario for a dual momentum investor. Why? Because it causes big problems in 2 separate phases.

Phase 1: the crash.

The crash itself will almost definitely hurt your dual momentum portfolio.

Unless the crash occurs in the midst of a bear market at a time when you have already divested of stocks or other high risk assets,you will feel the full weight of the flash crash’s destruction.

It will be difficult to tell your portfolio from that of a 100% “risk on” stock portfolio on the day of the crash.

But if you are anything like me, it will be worse than that. After all, dual momentum’s primary attraction is it’s a promise of diminished drawdowns with unfettered returns. But here is an instance when “temporal diversification,” offers none of the benefits of plain old asset class diversification. In this instance, the dual momentum investor’s portfolio is indistinguishable from that of a 20 year old stock trader who wants big rewards for taking big risks. In other words the concentration of stocks within the portfolio at the time of the crash creates a bad mismatch between investor risk tolerance and portfolio risk.

But don’t worry, it gets worse…

Phase 2: the recovery.

If the flash crash is a plain old panic such as what was seen on Black Monday in 1987, then the market will react rationally afterwards, and prices will bounce back relatively quickly. Equities will soon recover to reflect their true value in the market.

So what would be expected is a very rapid drop, followed by a pretty rapid recovery.

This is the truly the worst case scenario for the dual momentum investor. For as soon as the month of the flash crash ends, the strategy will dictate the selling of high risk assets and the buying of safe assets. So just as the market begins its recovery from its hick-up, the dual momentum investor will be on the sidelines, losses locked in.

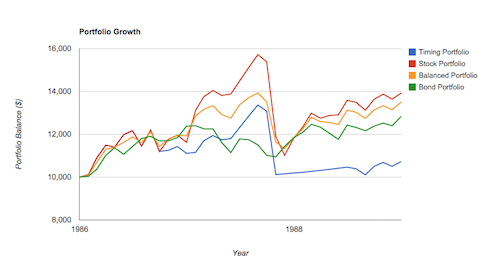

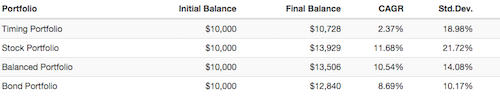

This nasty scenario really poses the same problem for any tactical asset allocation strategy including the 200 day moving average approach. (And frankly I lack the back testing tools to display an isolated look at this time period with dual momentum) so let’s look at the years surrounding Black Monday using a 10 month moving average strategy with the S&P 500.

(Tough coupla years for trend following…)

Take home: flash Crashes are kryptonite to trend following strategies like dual momentum.

One could come up with strategies to avoid this doomsday scenario, such as filtering out large single day drops in bull markets, but since there’s only been one black Monday in our history, it would be impossible to test such a strategy in any meaningful way. So my feeling is that it is wiser to take the bad with the good and stay true to dual momentum even should such an event occur again in the future.

I comfort myself with the rarity of such events in the past in contrast to the pervasive outperformance of dual momentum in long term backtesting.

So flash crashes are absolutely a risk to be aware of and to prepare oneself for psychologically.

But they by no means the only risk….

There Is Also The Risk Of Whipsaws.

Imagine you’re a dual momentum investor who uses 12 months as your look back period.

Now imagine the market slowly trends down over 12 months erasing the prior year’s gains. On the 12th month in keeping with the strategy you convert to a risk-free asset such as short term treasuries which have just begun to outperform the alternatives in your portfolio. As luck would have it the market starts to rally shortly after you move to the sidelines.

And several months later, when prices recover enough for you to become fully invested in stocks once again, the stock market once again takes a turn for the worse.

In this scenario you are “risk on” when the market goes down and “risk off” when the market goes up. Your timing is perfectly out of sync with the market. Never a good place to be.

This turn of events is termed a “whipsaw”. And it can be a random but destructive turn of events for a tactical strategy such as dual momentum.

Take-home message: market whipsaws when perfectly out of sync with the momentum look back period can be very disruptive for the dual momentum practitioner.

One way to avoid this risk would be to use multiple look back periods when implementing your dual momentum strategy. For instance you could manage one third of your portfolio with a three-month look back, one third of your portfolio with a six-month look back, and one third of your portfolio with a 12 month look back.

This is probably something worth considering. The main downsides to such an approach would be the increased complexity, and the increased trading costs (both in terms of commissions and bid ask spreads.)

Hypothesis 3: Short-Term Treasuries Are A Risk-Free Asset.

Counter argument: risk-free assets are only risk free until they are not.

I’m fairly certain that during the time of Alexander the Great, Greek government debt must have been considered “risk-free.”‘ The same must certainly have been true of Rome under Julius Caesar. Since Greek and Italian debt is no longer considered “risk-free,” the lesson is clear. There is no such thing as a risk-free asset. With time every asset is risky.

But the day that US short-term treasuries become a risky investment will be bad news for almost every investment class and approach, not just the dual momentum strategy. So while this is a real risk, it’s a tough one to hedge against regardless of your investment approach.

So those are some the risks that I can perceive lying out there waiting for me as a dual momentum investor. But I’m quite certain these are not the only risks. They are simply the ones that I can conceive of at this point in time.

Since I’ve chosen to go down this avenue, it is fairly obvious that I like the rewards of this approach enough to knowingly take on these risks. But if there are other risks to dual momentum that concern you, by all means share them below.

Because as Sun Tzu points out the more we know about our own weaknesses and strengths and as well as those of our competitors, the less we have to fear.

15 Responses to “Looking Under Rocks”