Market timing is for the birds. Except of course, when it isn’t.

Tonight I thought I would write about one of my favorite investments.

Interestingly, it is an investment that I do not hold much of a position in right now.

Which kind of makes me a market timer. But I’m getting ahead of myself.

TIPS is an acronym for treasury inflation protected securities. And these are a special type of bond that is issued by the US government, (and other governments.)

You will recall that bonds in general are just investments in debt. The bond owner lends a government or a company or a person some money and in exchange is promised an interest payment on that money for the life of the loan in addition to a term of repayment on the principal.

And TIPS are the same thing with one important distinction. The value of the principle (the amount you will be paid back at the end of the term of the bond) changes with inflation. So if an inflation index (like the CPI in the case of United States TIPS) goes up, so does the amount that the that government owes you in terms of both principal and coupon.

(Since the principal moves upwards and downwards with inflation, so does the coupon (since it is by definition simply a percentage of the principal.)

And this is not a small distinction. This inflation adjustment means that if you are promised a real return of 2% for the entire term of the TIPS, you will get exactly 2% on your investment in buying power for the term of the bond.

If inflation goes up, you are not at all affected, and even if inflation goes down (ie deflation) you are positively effected, since even in the setting of deflation the principal that the government owes you can never go down below the value of your initial investment (nor can the interest payments since they are always tied to the inflation adjusted principal.).

So if you purchase a 30 year TIPS with a coupon of 3% this means that your invested money will be backed by the full authority of the US government (virtually no credit risk) and that you will get a real 3% return on your investment for 30 years.

Short of an FDIC backed bank account below $250,000 there is really no more secure of an investment than TIPS.

That being said it is important to know the playing field. So here are some useful facts to know about TIPS.

- TIPS are best held in tax sheltered accounts since the interest adjustment on the principal will be taxed as capital gains, and the interest payments when adjusted upwards by inflation, will be fully taxed as dividends.

- TIPS can be purchased from the treasury at auction (but not in tax shelterred accounts.)

- TIPS can be purchased through a brokerage for tax sheltered accounts.

- TIPS are quite liquid and can be resold, though their value changes with interest rates,

- I-bonds represent a more tax efficient way of investing in inflation protected securities within taxable accounts.

- You can only buy 10,000 dollars worth of I-bonds per year per person.

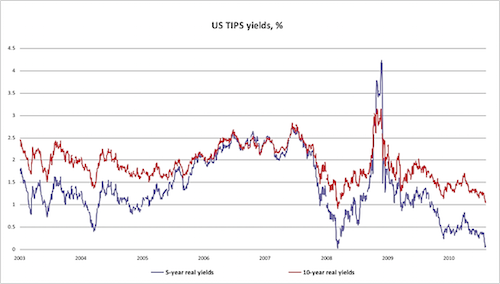

- The historical spread on long term TIPS yields have ranged between 0.125% and 4% coupons.

So let’s think about some ways to use TIPS intelligently in your portfolio.

You have won: so stop playing the game.

If you hit “your number” and the TIPS rate is 4%, you can invest your entire stash in TIPS and lock in your current lifestyle for up to 30 years at virtually zero risk. If inflation goes up? No problem; so will your coupon which is what you are living off of.) And if there’s deflation? No problem you actually make money on deflation. The value of the dollar goes up and you get paid a fixed payment for 30 years.

And at the end of the run if you have just lived off of the coupon payments, you will be exactly as rich 30 years later as you are at the beginning of your term.

De-risk your portfolio.

If you’re getting close to your goal for retirement then when TIPS rates get high, a smart move is to increase your portfolio’s bond allocation, and to fill your bond bucket with long term TIPS. This allows you to do two important things. The first is that by using high-yielding TIPS you’re getting equity like returns from a safe asset. And the second thing is that by increasing your allocation to bonds you are drastically reducing your downside risk. In other words, if the stock market collapses your portfolio will be less effected and your wealth will be preserved. So you’re basically maintaining your expected return from your portfolio, and drastically decreasing your risk of loss.

A bird in the hand.

If you are early in your career and working on accumulating a nest egg for a distant retirement, it probably doesn’t make sense to increase your bond allocation significantly just because TIPS rates go up. The fact is that over long time horizons equities are usually expected to return more then bonds because they are riskier.

But in this event, whatever your predetermined bond allocation is, you should consider filling it with long-term TIPS.

And there are a couple reasons for this.

The first is that as interest rates go down the value of the TIPS that you have purchased will go up. So you can sell them at a premium and take a profit.

And the second reason is that 4% real-year-old from your bonds is never a bad thing!

Build your own annuity

One neat thing you can do if you have a large supply of tax shelterred cash is to buy a TIPS ladder.

What this means is that you buy tips in the amount of your yearly expenses for up to 30 years into the future.

In doing this you know that each year one of your TIPS will mature and you can use that principal to live on.

What you’re doing is essentially taking your living expenses and putting that amount in a Time Machine and sending it out up to 30 years into the future for when you will need it. And the nice thing about this approach is that your living expenses will automatically be adjusted for inflation.

The other nice thing is that all of these TIPS will be spitting off interest payments (coupons) every six months which you can invest in anyway you like. (Go ahead and roll the dice you have an annuity.)

Here is a nice post on the philosophy of the TIPS ladder.

And here’s a nice post on how to actually construct your own TIPS ladder.

So now that I’ve (hopefully) convinced you that TIPS are something to keep an eye on for future opportunities, let’s get to the market timing peace.

Larry Swedroe suggests a sliding scale allocation to TIPS within the bond allocation of your portfolio.

And the idea here is pretty simple.

Since we know that the historical range of TIPS yields is somewhere between 0.125% and 4%, we will always be able to recognize when TIPS are cheap. (The higher the yield, the cheaper the TIPS.)

So when long term TIPS are offering a 4%-yield (like in late 2008), obviously all of your bonds should be in TIPS. (A 4% real risk-free return can really rarely be beat.)

If on the other hand, TIPS are offering a 0.125% yield, (like now) you probably shouldn’t bother. The yield will inevitably go up at some point, and when it does the value of your TIPS will go down.

So in other words the higher the TIPS yield, the greater the percentage of your bond allocation which should be in TIPS.

This strategy essentially ensures that you will buy low and sell high on your bonds. (Always a good idea.)

So market timing in this way is a low risk, high reward affair which I would recommend that you keep in mind for the future.

One of these days I will surely announce “I’m going all in TIPS for my bond basket.”

And my hope is that when I do, you’ll both know what I’m talking about, and at least consider it for yourself.

4 Responses to “Visible Iceberg Parts”