So if our overarching goal here is to win big by avoiding big downward movements in the value of our investments, we have already covered some pretty decent ways of achieving this.

In my most recent post in this series, I discussed the value anomaly and the idea of buying companies at stock prices well below the underlying asset liquidation value of the company in order to create a floor to minimize the risk of the permanent loss of capital, even in the case of company bankruptcy.

But the more conventional idea to avoid the destructive loss of value in your portfolio is to diversify.

And that idea is quite intuitive. Instead of putting all of your eggs into one basket and going 100% US stocks, you create a variety of baskets with different unique assets that all react differently to different market environments.

Some US stocks here, some international stocks there, a bunch of bonds over here, perhaps some commodities sprinkled in there, some cash and some real assets like real estate here, maybe even some precious metals for good measure.

Diversification is like a box of chocolates

And in doing so you accomplish a number of things.

- You decrease the volatility of your portfolio by always having some assets zigging as others are zagging.

- No matter how badly the overall economy is doing, at least one of your assets should always be doing decently.

- By rebalancing you are able to buy cheap assets and sell expensive ones.

But let’s think about this further. If we choose to list the upsides, shouldn’t we also list the downsides of diversification?

- No matter the market conditions, there will always be some asset class you own that will perform badly. (in the current market, commodities would be a good example of just such a dog.)

- By having to own many baskets you limit your exposure to the baskets that are likely to bring the highest return long term. (I.e. You’ll never have enough stocks in a bull market.)

- Despite mixing all of your baskets together, your returns will still largely be determined by the most volatile asset. (I.e. you will always have too many stocks in a bear market.)

Which brings me to today’s strategy: trend following.

Trend following is truly just a fancy name for systematic market timing. But it’s allure is obvious.

Why not just own stocks when the market is going up, and cash or short-term bonds when the market is going down? With such an approach we can get rid of many of the negative aspects of diversification. In fact I think of trend following as “temporal diversification.” Ie instead of owning 60% stocks and 40% bonds 100% of the time, you own 100% stocks for the 60% of the time when the market is going up, and you own 100% short-term bonds for the 40% of the time when the the market is going down.*

But there are number of reasons to be suspicious of any market timing scheme.

- Most importantly: predicting future movements of stock prices is probably impossible.

- Switching positions instead of buying and holding means more trading, which means more costs and “friction,” and compounded costs are very destructive to your wealth.

- Trading in taxable accounts can lead to taxable events which will diminish the compounding effect overtime.

- Changing positions based on your intuition or gut feelings on where the market is going is almost always a very bad idea.

Which brings us to quantitative market timing, and the idea of moving averages.

So what is a moving average?

The moving average is simply the average price of an asset over a look back time period. So for a 10 day moving average you would add up the closing stock price for the past 10 trading days and divide by 10.

And the classic use of a moving average is essentially to determine momentum. Although day to day securities move up and down seemingly at random, the moving average allows us to see the smoothed trend of the securities’ price.

And since security prices usually trend upwards up unless there is a headwind, we generally expect that today’s price to be above the 200 day moving average unless there is negative momentum. And because the momentum anomaly tells us that assets that have recently done well are more likely to continue to do well (and vice versa,) owning only recent winners tilts the odds slightly in our favor.

So one systematic approach to trend following is to hold an asset as long as it’s current price at the end of the month is above its 200 day moving average. But when the security’s price dips below it’s 200 day moving average and stays there at month’s end, one trades out of the position to a safe asset like short-term treasuries.

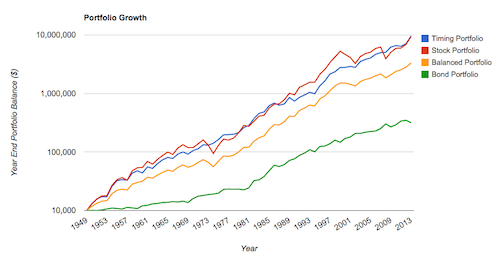

And how does this approach work? Pretty well actually. Let’s take the example of an S&P 500 index fund traded based on it’s end of month 200 day moving average.

Observations:

- The moving average portfolio (blue) returns as much as a 100% S&P 500 portfolio(red), with much less volatility and much smaller drawdowns.

- The moving average portfolio actually has less volatility and smaller drawdowns than the “balanced” 60/40 stock/bond portfolio (yellow).

- The moving average portfolio performs comparatively best when the market is at its worst.

- The moving average portfolio is less correlated with the stock market than the balanced portfolio!

- The flash crash in 1989 was not kind to the moving average portfolio.

So all in all such an approach is pretty reasonable.

Personally I do not use this strategy, but it is probably my second favorite investment strategy.

In terms of first principles it hits all of my touchstones for investment.

- It is simple to implement and easy to understand.

- It is implementable using only low-cost index funds.

- There is a minimum of trading.

- It is rules-based, not emotion-based.

- It is based on a persistent and robust observation that rings true to me and that I believe will persist (the momentum anomaly.)

And at least historically, the strategy has done a very good job of avoiding large losses in bear markets.

As always, comments welcome!

* percentages pulled out of thin air here.

5 Responses to “Getting Trendy”