I’ve discussed credit card churns and flexibility, and reconsideration calls and keeping your newly approved cards organized….

On to the fun world of spending lots of money without spending much money at all: otherwise known as manufactured spending.

1. What is Manufactured Spending?

Before covering the specifics of how to manufacture spending, it’s probably useful to start with a first principle.

Like…

What in the hell is manufactured spending?

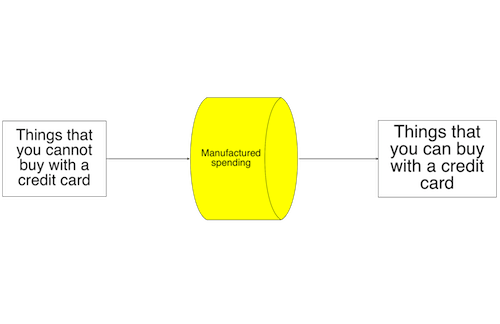

Manufactured spending can really be defined with a simple three box flowchart.

If you could put every cent of your spending on credit cards, there would be virtually no churn whose bonus requirements you could not meet just by paying yours bills.

Sadly your biggest bills, like mortgage and student loan payments cannot be paid simply by credit card.

So at its most basic you can use manufactured spending to shift non-credit card eligible spending onto my credit card. And if you can do that, you can probably spend a lot of money on absolutely nothing without really spending much at all.

Manufactured spending is not unlike the mythical barrels that alchemists placed lead into in order to convert it into gold. It transforms useless payments that would be otherwise be paid by check or cash into useful credit card spending.

For instance, just using a simple (and soon to be discussed below) method of purchasing Visa Gift Cards and loading them onto a Go Bank Card you would be able to manufacture $6,000 a month for only a 1% fee (or 60 bucks) using a Gobank account for both you and your spouse.

How many credit card bonuses can that $72,000/year of manufactured spending just from ONE source earn you? At an average $3,000 minimum spending requirement on each, that’s 24 credit card bonuses or around 1,200,000 miles . At 2 cents per point that’s $24,000 of free travel and it would only cost you $720 out of pocket (1%) and some trips to stores like CVS/Rite-Aid/Walmart.

On the other hand, manufactured spending is a constantly evolving process as old opportunities close and new ones arise, so it is always wise to have at least 2 useable techniques at your disposal at any time. This will make your strategy robust to the inevitable changes to come.

2. Visa Gift Cards for Manufactured Spending

To start the glorious chain of events that results in manufactured spending, begin with the mundane.

We simply take our new credit card to a store (or online) and buy a Visa gift card.

Why a Visa gift card?

Well, sometimes it can be a MasterCard gift card, but in general it should not be an American Express gift card. This is because by law, any card with a Visa or MasterCard logo (but not an American Express logo) must be able to accommodate a PIN number. And PIN numbers are required in order to reload prepaid cards later. (Don’t worry we’ll get there soon.)

Visa cards are preferred over Mastercards based on reports of difficulty using MasterCard gift cards to reload prepaid cards at Walmart.

In any case buying Visa gift cards using a credit card is hardly rocket science.

But what is simple is not always easy, and here are some of the roadblocks that you may encounter on this first simple step of your journey:

Hardwired cash registers

Sometimes you simply will not be able to buy some gift cards at some stores as the checkout system is programmed not to allow credit card purchases of gift cards. (Personally, I have often had good luck at RiteAid, Walgreens, CVS, major grocery stores, and online gift card retailers, but it’s an ongoing trial and error process.)

Suspicious check out personnel

Some employees are suspicious of multi-thousand dollar purchases of gift cards (which I get**.)

My usual policy is just to be honest and pleasant and act like I have nothing to hide (because I don’t.) But for some people the social discomfort of navigating such a dynamic can be too much. For those sensitive souls, I would recommend purchasing gift cards online.

Dealing with shipping, insurance etc.

When you purchase gift cards online, there is a significant delay between purchase and actually receiving the card. This is somewhat less efficient than simply walking out of a store with plasticized cash. Furthermore,there is always the risk of the card getting lost in the mail, so you must sometimes pay extra for insurance, deal with Postal Service hassles etc.

(That being said It can be a great ((and inexpensive)) option to order online. If you want a nice review of some options for purchasing gift cards on line check out this article.)

But there’s not too much more to securing gift cards than those minor inconveniences. And the rewards of buying cash equivalents are significant.

When you first start browsing gift cards, you will find a dizzying array of choices. Which raises the question: which cards should you buy?

When choosing a gift card the main factors that I consider are the

- Fees to activate the card

- Whether or not I can set the PIN on first use (as opposed to having to call a phone number to set the PIN)

- And whether or not it can later be used for my intended purpose (ie Walmart reloads, moneyorders, etc….)

Some of the Visa cards that we have personally purchased are itemized below. These represent only own anecdotal experience. This is not an exhaustive list, and we make no claims about the validity of these descriptions, other than to say that they are described in good faith and honesty. Please double check these facts. As always, Buyer (reader) beware!***

Vanilla Gift Card, Vanilla Visa, Onevanilla

Fee: $4.95

PIN: set on the first use

What we now use them for: Purchasing money orders. (These used to be very useful when Walmart and Target accepted them, now they are much less of a find.

Limitations: Walmart registers are now hardcoded not to allow you to reload your Serve/Bluebird card with any vanilla gift cards, so if Walmart is your plan, avoid any Visa gift card issued by Vanilla!

US Bank Visa gift card

Looks like this (only its a Visa, not MasterCard)

Fee: $5.95

PIN: Call in to set.

What We use them for: these are ubiquitous in grocery stores. Supermarket purchases can be geographically convenient, or economically useful when it comes to gaining fuel rewards. You can still use these to load Gobank cards.

Limitations: A little bit more expensive than a 1% activation fee, as with vanilla cards.

General Wisdom

One detail worth remembering when you do pull the trigger to purchase your gift cards are to always keep your receipts, (at least until you liquidate the cards.)

A good habit is to wrap the receipt around the gift cards that you have purchased and to file it all away once you have liquidated the card.

The reason is that at some point you will buy a gift card and it will fail to activate.

When this happens, you may be faced with the possibility of losing thousands of dollars (an unpleasant prospect, to say the least).

But in my experience I have never lost any money manufacturing spend. The worst outcome has merely been being unable to access my cash for a few weeks or so, and having to deal with crappy gift card company customer service on the phone. But in the end, armed with my receipts it all turned out okay (thus far).

And the best part is that once you’ve made your purchase you’re that much closer to hitting your lofty credit card spending bonuses, which will net you thousands of dollars worth of free travel.

One concern that always comes up is whether or not buying gift cards constitutes a cash advance. To date I have never been charged a cash advance fee for such a purchase. My guess is that it is unlikely I ever will. As it stands now, a $1000 purchase of gift cards at a drugstore simply looks to the credit card company like a thousand dollar purchase of something at a drugstore.

While banks may know where you shop, and how much you spend, they currently have no way of knowing what you bought. Frankly, I’m not sure they will ever have that ability as it would constitute a significant invasion of consumer privacy. But who knows?

In any case you are already aware that it is always a good idea to set your cash advance limit to zero when you activate your credit cards,which pretty much eliminates the risk of being charged the dreaded cash advance fee.

*It is possible to manufacture spend with American Express gift cards. Which is beyond the scope of this discussion.

**If you spend your day selling two dollar gum packs and three dollar bags of chips, a single credit card purchase of $2500 worth of gift cards is quite eye-catching, which is in and of itself suspicious. Furthermore some criminal types do use gift cards for actual money laundering.

***It is always a good idea to Google a new gift card before purchasing it. Flyertalk and blogs will often have useful information about the card in question. And a simple smart phone search while in the store can save you a lot of hassle later.

Action Steps:

- Go to local Drugstores, office supply stores, and Supermarkets and check out what Visa gift cards are available and in what amounts.

- Figure out what percentage of the the maximum loadable gift card amount the activation fee represents. What is your cheapest option?

- Study (and bookmark) this page to research the gift card landscape available.

- If you find a different gift card that works for you (or not), help us to expand the database by emailing a picture of it to us along with;

- Where you bought it.

- What bank issues it.

- How much was the activation fee.

- What prepaid card you loaded it on. (Or failed to load it on.)

3. How to use Reload Cards for manufactured spending

We talked above about the psychological and practical barriers to purchasing the gift cards, and important factors to consider when choosing your weapons.

Now we will talk about a corollary to the purchase of Visa gift cards: the pursuit of reload cards.

The issues are very much the same, hardwired registers, suspicious cashiers, social isolation, but the products are meaningfully different.

Simply put reload cards are far superior to Visa gift cards.

What is a reload card?

A reload card is another cash equivalent product that is used to transfer cash from a credit card onto a prepaid card.

The difference is that with a reload card you can load the cash directly on to your prepaid card without actually visiting a store. Goodbye Walmart, hello smart phone.

So instead of the possibility of two suspicious cashiers (One where you bought you Visa gift cards, and one where you loaded it onto your prepaid card), with these, there is only the possibility of one suspicious cashier (where you purchase your reload card.)

More importantly, instead of spewing hydrocarbons, making your way to a megastore in boxy-big-box-land, you can stroll around your neighborhood sipping home brewed coffee and stretching your legs*.

What reload cards are out there (that I have personally used)?

1. Reloadit cards

Cost to purchase: $3.95

Maximum load: $500.00

The good: They are cheap. The card fee of only 0.4% to load $500 is pretty good.)

The bad: it can be very difficult to buy them with credit cards.

Where I have had luck purchasing them: sporadic Safeway stores.

What I have used them for: Loading a Rush prepaid card. You can also use these to load your Serve card (but you will eventually get shut down by Serve). For a more complete list of prepaid cards that you can load with Reloadit cards, see here.

Action Steps:

Figure out if you can buy Reloadits with a credit card locally. If you can, you are in luck!

4. How to Use Prepaid Cards for Manufactured Spending

Today we get to the crux of the matter. If manufactured spending is alchemy, turning credit card spending into cash, then the transformational step is certainly the loading of your prepaid card which is not much more than a pseudo-checking account.

What is a pseudo checking account?

A pseudo checking account is a prepaid card that can be loaded by credit card in a number of ways. (We’ve already discussed using Visa gift cards, and reload cards,and both of these can be used to load prepaid cards.)

Pseudo checking accounts were conceived of as a way to take advantage of err… as a way to bring the power of checking to the unbanked masses.

The idea is that those who do not have the resources to open bank accounts can simply register for a prepaid card and then use it to write checks and do online shopping. Sure, there are often a lot of little fees, but the fees are nowhere near as bad as at those check cashing places. (Plus the prepaid cards drive these customers into establishments like Walmart and Target.)

The important thing, from a miles game player’s standpoint, is not the societal implications of such a product. The important thing is that the prepaid card can be used to transform credit card spending into cash equivalents (checks, money orders, and direct withdrawals to personal bank accounts.) This is really raison d’etre for manufactured spending.

There are countless pseudo-checking accounts, and we will write about a few of them here, though our list is not exhaustive.

If you research prepaid cards you will hear a lot about “Redbird, and Bluebird and Serve.” Sadly these once great products died as useful tools of manufactured spending one by one, and will no longer be covered here.

So you’ll have to choose your weapon.

Choosing a Prepaid Card

1. GoBank Card:

(The last card standing)

Gestalt: New applicants now have to pay an onerous $8.95/month fee to have this card. But with direct deposit of $500 a month this fee is waved.

Gestalt: New applicants now have to pay an onerous $8.95/month fee to have this card. But with direct deposit of $500 a month this fee is waved.

How To Load: swipe reloads at Walmart with non Vanilla issued visa gift cards.

How to unload: Use the clunky online bill pay to pay your bills, credit card and otherwise, purchase money orders.

Load limits: $2500/day, $3000/month

2. Rush Card

https://www.rushcard.com/

RushCard: This card has two plans. One has a monthly fee ($7.95 without direct deposit and $5.95 with direct deposit. The other one plan has a “pay as you go” fee. This second plan charges $1 per purchase up to a max of $10 per month.

How to load: direct deposit, checks, mobile deposit via Ingo Money, swipe reloads with Visa gift cards at Walmart Rapid Reload $3.74 fee. (non-vanilla brand Visa gift cards only.)

How to liquidate: Use online bill pay to pay your bills, credit card, purchase money orders, or use anywhere a visa debit card is accepted, ATM (free at MoneyPass)

Load limits: $1000/24 hours via reload cards/swipe reloads

3. AccountNow

https://www.accountnow.com/

AccountNow: Activation fee of $4.95. Monthly fee $9.95 for the AccountNow Gold Prepaid.

Get a $15 bonus with qualifying direct deposit of at least $500 in two or more consecutive months Bonus has to be redeemed by phone at 877-553-3767 within 30 days of meeting qualifications.

* If you go with AccountNow make sure to get the Visa prepaid debit card.

How to load: Reloadit ($3.95 fee), swipe reloads with Visa gift cards at Walmart, Walmart Rapid Reload $3.74 fee. (non-vanilla brand Visa gift cards only.).

How to liquidate: Use online bill pay to pay your bills, credit card, purchase money orders, or use anywhere a visa debit card is accepted, ATM (fees may apply)

Load limits: $1500 a day via reload cards/swipe reloads, $95000 a month limit. Cash loads limited to 5 per day and 30 per month.

4. PayPower Prepaid Visa

https://www.paypower.com/

PayPower Visa Prepaid: monthly fee of $5.95, load fees of $3.95 (may vary by retailer).

How to load: Reloadit ($3.95), Visa Readylink

How to liquidate: Use online bill pay to pay your bills, credit card purchase money orders, or ATM (fee may apply).

Load limits: $2,500 a day

5. Kaiku Visa Prepaid Card

https://www.kaiku.com/

KAIKU Visa Prepaid: No activation fee, usage fees, free Allpoint ATM withdrawals. Monthly fee of $3, cash reload fee $2.95-$4.95.

How to load: Walmart Rapid Reload $3.74 fee.

How to liquidate: Use online bill pay to pay your bills, credit card purchase money orders, or ATM ($500 per day).

Load limits: $950/day for Visa Readylink (7-11, Safeway)

Action steps:

- Choose one (or more) of the above prepaid cards as your weapon of choice. Start with the Gobank card.

- Apply for your chosen card.

5. Using money orders for manufactured spending

The miles game can seem a labyrinthine map of intersecting roads, highways and thoroughfares.

The main interstate runs from the purchase of gift card/reloadables to the loading of the prepaid card, to the paying of bills with the prepaid card.

But aside from this main thoroughfare, there are lots of side roads, scenic routes, and diversions.

And if that is true then today’s maneuver, leveraging money orders, is almost certainly like a highway rest stop.

Money orders are not the main event, but they are ubiquitous, and very useful, and when you need them (like 90 minutes after consuming a Big Gulp of Jolt Cola,) they are a godsend.

What is a money order?

To quote the only source that matters, Wikipedia:

A money order is a payment order for a pre-specified amount of money. As it is required that the funds be prepaid for the amount shown on it, it is a more trusted method of payment than a cheque.

So it’s kind of like a cashier’s check without the bank.

How does it work?

- Purchase a Visa gift card with a credit card. (Or use a prepaid card that you have previously loaded)

- Go to a big box store, grocery store, convenience store, post office… and purchase a money order with some form of a debit card/gift card using a PIN.

- Make the money order out to yourself, and deposit it in your own bank account.

- Rinse and repeat.

But there are other considerations:

Because of their ease-of-use, money orders are prime candidates for abuse by money launderers. Sufficed to say, manufactured spenders have no intention of laundering money, but it is better to never be suspected of such a thing.

There are laws against depositing more than $10,000 in money orders in a bank account in a month, and of breaking up a large amounts into multiple deposits in order to avoid running afoul of the $10,000/month limit.

As an example, one cannot deposit $7000 one day and $5000 another day into a bank account in order to avoid being flagged as having deposited greater than $10,000 in money orders in a single month: this is an actual crime on the books known as “structuring.”

Consequences of the overzealous use of money orders could include:

- Having your bank account shut down

- Having your assets seized

- FBI investigation

How to Use Money Orders Legally

Here are some simple rules that I abide by in order to avoid running afoul of the law when using money orders:

(Note: These represent my own personal practices and represent no guarantee against you running into trouble.)

- I have never purchased more than $2000 in money orders at one time.

- I no longer deposit money orders into my main bank accounts, as I do not wish to have these at risk of being shut down.

- I would never deposit more than $2000 in money orders in a day, or $10,000 in a month into any one bank account.

- I have opened a separate account simply for money order deposits.

In terms of this last point, when choosing a bank to deposit your money orders in, it is useful to know the playing field.

What you really want is a bank that will

- Allow you to deposit money orders without any hassle or shutdowns.

- Allow you to deposit money orders using mobile deposit (on your smart phone.)

- Not have future lucrative credit card offers that will be out of your reach should your account be shutdown.

According to a Flyertalk wiki the following banks have the capability to have money orders deposited into them by mobile phone:

- Simple

- Everbank

- Discover Bank

- TIAA bank

- UFB Direct*

- Citibank

- Wells Fargo

- DCU

- USAA

- LMCU

- PenFed

- Eastern bank

- BBMT

How have I used money orders in travel hacking?

- I have really only ever purchased money orders with visa/MC gift cards previously purchased by credit card.

- Before my paypal account was shut down, I considered purchasing them with my PayPal Business Debit Card,(which would allow me to use the full $4000/month Mycash load limit…and even with the $.79/$1000 money order purchase fee, it would still be better than free.)

- It would seem possible to purchase them with a prepaid card (i.e. Gobank, T Mobile), though I’m not sure why one would ever want to do that, since you can just withdraw the money in these accounts directly to your bank accounts.

All in all money orders represent a nice little escape hatch that one can use anytime one gets stuck with a gift card that didn’t work for its original intent.

So maybe money orders are not so much rest stops as runaway truck ramps?

Who knows.

But they are exceedingly versatile…

Kind of like a swiss army knife nestled delightfully between a runaway truck ramp and a rest stop….

In any case the point is that they are damn useful (if you enjoy flying places for free.)

Action Steps:

- Check out the money center at your local supermarket, bigbox store, and post office. Who has the best prices?

- Ask if you can purchase money orders with a debit card.

*My choice

6. How to Manufacture Spend Without Spending a Dime

In the field of manufactured spending one of the most common metrics is “cents-per-mile-earned.”

The idea here is that if you’re doing manufactured spending, there are always some costs associated with the exercise, and those costs can be quantified if you divide the total cost of the manufactured spending in cents by the total number of miles earned.

As an example, let’s say you bought $2000 in Vanilla Reloads Card at a CVS with your Chase Sapphire Preferred card.

Each $500 vanilla reload card costs $3.95 in activation fees. There’s no category bonus on spending on the Chase Sapphire Preferred card at drugstores, so each dollar spent yields one Ultimate Rewards point.

So the calculation goes something like: (395 cents X 4) /2000 Ultimate reward points = .79 cents/per Ultimate reward point earned.

Not bad. But can we do better?

As you have undoubtedly picked up by now, I (Alexi) am not just a miles enthusiast. I’m also an early retirement enthusiast.

So the idea that costs (even those less than 1%) matter in the long run, is something that I feel deep in my bones.

Because of this heartfelt belief, I do everything I can to avoid paying anything at all for manufactured spending.

There are undoubtedly thousands of ways to manufacture spend for free, but I will highlight the ones that I have used myself.

1. Fuel Points.

Last summer QFC supermarkets in my area ran a promotion where for each hundred dollars you spent in store, you received 10 cents off per gallon of gas at Shell stations (up to one dollar off per gallon.)

Fortunately visa gift cards counted towards fuel points. So each thousand dollars of spend on Visa gift cards cost me about $12. But I then got one dollar off per gallon on a fill up. With my 18 gallon tank this netted me six dollars positive for each thousand dollars of manufactured spend. In other words I was making .6 cents-per-mile-earned.

2. Gift Card Mall through a cash back portal.

By going to a portal finder like cashbackmonitor.com, you can find cashback on Visa gift card purchases from portals such as topcashback.com for outlets like giftcardmall.com.

The cost of manufactured spending usually hovers around one cent per mile, but there is a cost to having gift cards sent to you. So anytime you get more than 2% cashback on such a deal you will likely come out ahead.

The main downside of this strategy is that there is a lag time between your purchase and receiving the gift cards. Kind of a hassle.

3. Subsidizing your gift card purchases with the concurrent purchase of gift cards with a cashback credit card.

This is my current go to strategy.

Often during credit card churns I will apply for a seventh card, not for the sign-up bonus, but for manufactured spending purposes. I call this extra card a “plus one.”

My favorite “plus one” is the old Blue Cash card from Amex (click here to learn more). After the first $6500 in spending a year, you get 5X cashback on all purchases at drug stores supermarkets, and gas stations.

So each time I go to put manufactured spending on my credit cards, I will buy $1-2000 worth of gift cards with my cashback credit card.

Each thousand dollars I spend in this manner yields $50 in cashback. This is more than enough to cover the purchase of $4000 worth of gift cards with my other miles earning credit cards. So the only cost is the opportunity cost of not earning miles with the spending on my cash back card. That’s a good trade for me, and my goals.

And these examples just scratch the surface of what is possible. The sky is the limit.

It is worth pointing out, however, that there are some additional considerations.

The idea of cents-per-mile-earned is only valid if you’re manufacturing spending simply for the sake of manufacturing spending.

If you’re manufacturing spending to hit a credit card sign up bonus then the cents-per-mile-earned becomes much cheaper.

You see, the consequences of not hitting your spending targets and missing tens of thousands of miles in the form of a signing bonus, means that you are actually earning far more than the calculated miles per cent from the above equation.

Simply put, manufactured spending is far more valuable when it enables you to hit many more credit card sign-up bonuses than you otherwise could with just your regular spending.

I wanted to jump in here quickly to stress how important that last point is to the overall strategy. If it costs you ~$25 in gift card fees to earn a 50,000 point bonus you value at $1,000, that’s a pretty fair trade!

Without these tactics one can earn about 500,000 miles/point per year but with them one can earn well over 2,000,000 per year. That 1.5 million mile/point difference is worth about $30,000 (if you value your points at 2 cents per point as I usually do). That’s $30,000 of tax free travel that a manufactured spender earns each year above what a conservative approach earns, because of manufactured spending.)

On the other side of the ledger there are additional costs of manufactured spending that are not accounted for in the above equation.

Gas is not free.

More importantly time is not free.

If you don’t enjoy the exercise of manufactured spending, you’re probably better off just spending your free time with your loved ones or participating in your favorite hobbies, rather than spending extra time to offset the costs associated with manufactured spending.

As hard as it is for me to understand, I admit that not everyone gets their kicks out of buying gift cards and designing model investment portfolios.

That being said, I hope this is an instance where you can gain some valuable insight from someone else’s fanaticism.

7 Responses to “Everything you need to know to manufacture spending”